Categories

Buyer, SellerPublished September 23, 2025

Federal Reserve Rate Cut: What It Means for You

With the Federal Reserve’s recent rate cut of roughly 25 basis points last week, it’s not likely we’ll see a significant drop in mortgage rates in the immediate short term. Mortgage rates don’t fall in lockstep with the Fed’s moves—since long-term factors like Treasury yields and inflation expectations also play a role—borrowing costs often ease at a modest rate over time.

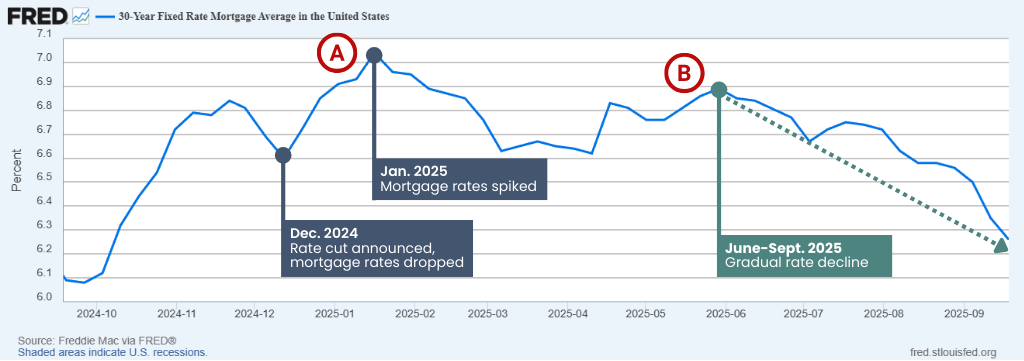

The chart below, from the Federal Reserve Bank of St. Louis, which manages the Federal Reserve Economic Data (FRED) database, indicates two mortgage trends in the last 12-month span:

A: The last rate cut in 2024 prompted an immediate drop in mortgage rates, but it spiked back to a new high in a matter of weeks.

B: In the second half of 2025, mortgage rates have been on a gradual decline, with the expectation that rate cuts were coming, and did happen last week. Given the Fed’s indication of two additional cuts before the end of 2025, we’re optimistic there won’t be another spike. Time will tell, and we’ll keep you posted.

As for a September market snapshot, the local market is steadily shifting to favor buyers, as inventory is elevated compared to last year and nearly 50% of active listings are seeing price reductions. For buyers, it’s important to have your list of must-haves in a home to focus your search. And, it’s key to have your financing lined up so you can make an offer when you find the home that checks all your boxes.

For sellers, we are seeing price reductions at almost every price point as homes linger on the market. That’s where strategic pricing, marketing, and negotiation are critical in ensuring you achieve the maximum value of your sale.

Keep an eye out for our October newsletter that will include a more in-depth market analysis for Q3 of 2025. In the meantime, if you have questions about the market or your home, let’s talk.

|

or another way